VC Split in Q1 2026: LPs Have A Powerful New Choice Now

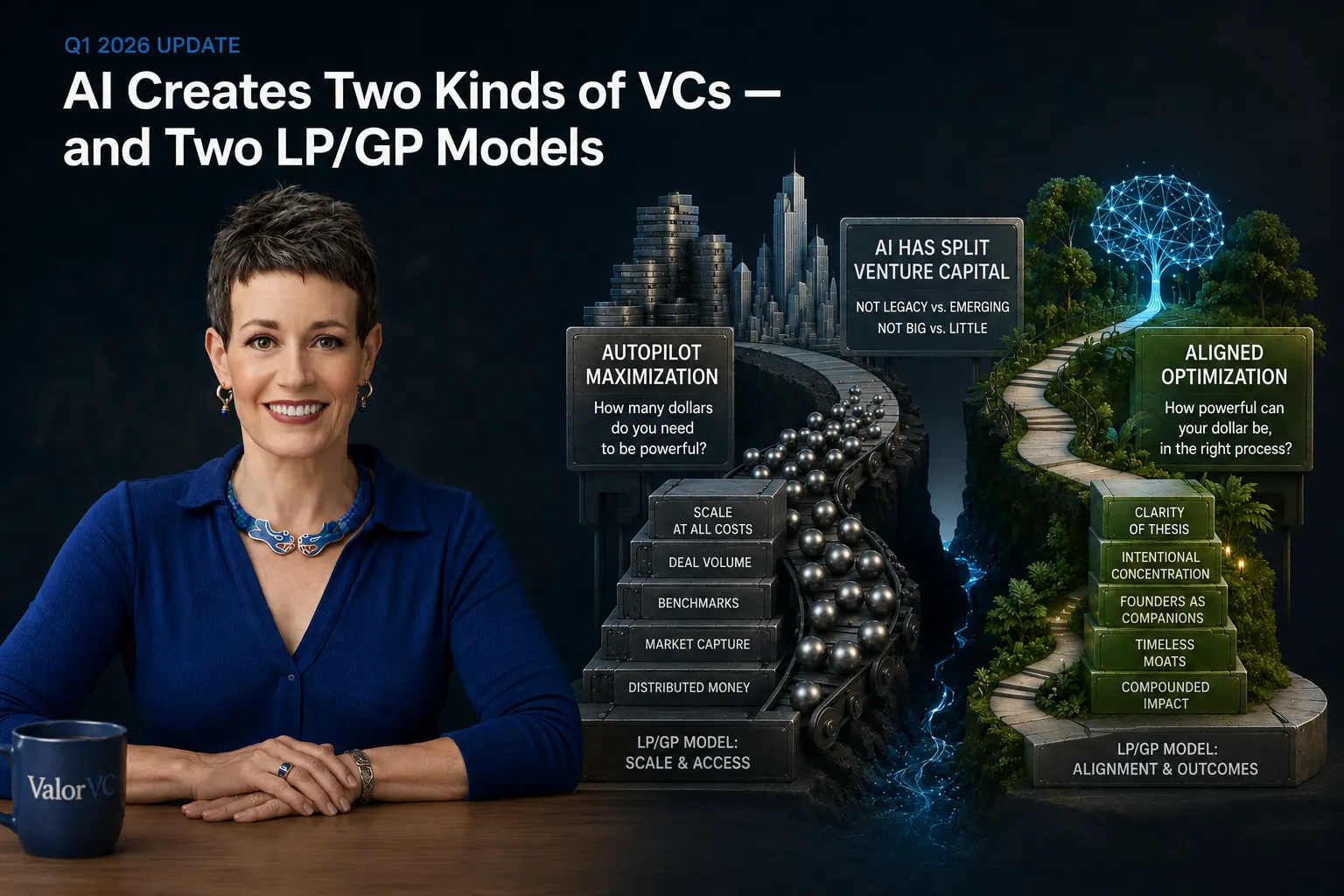

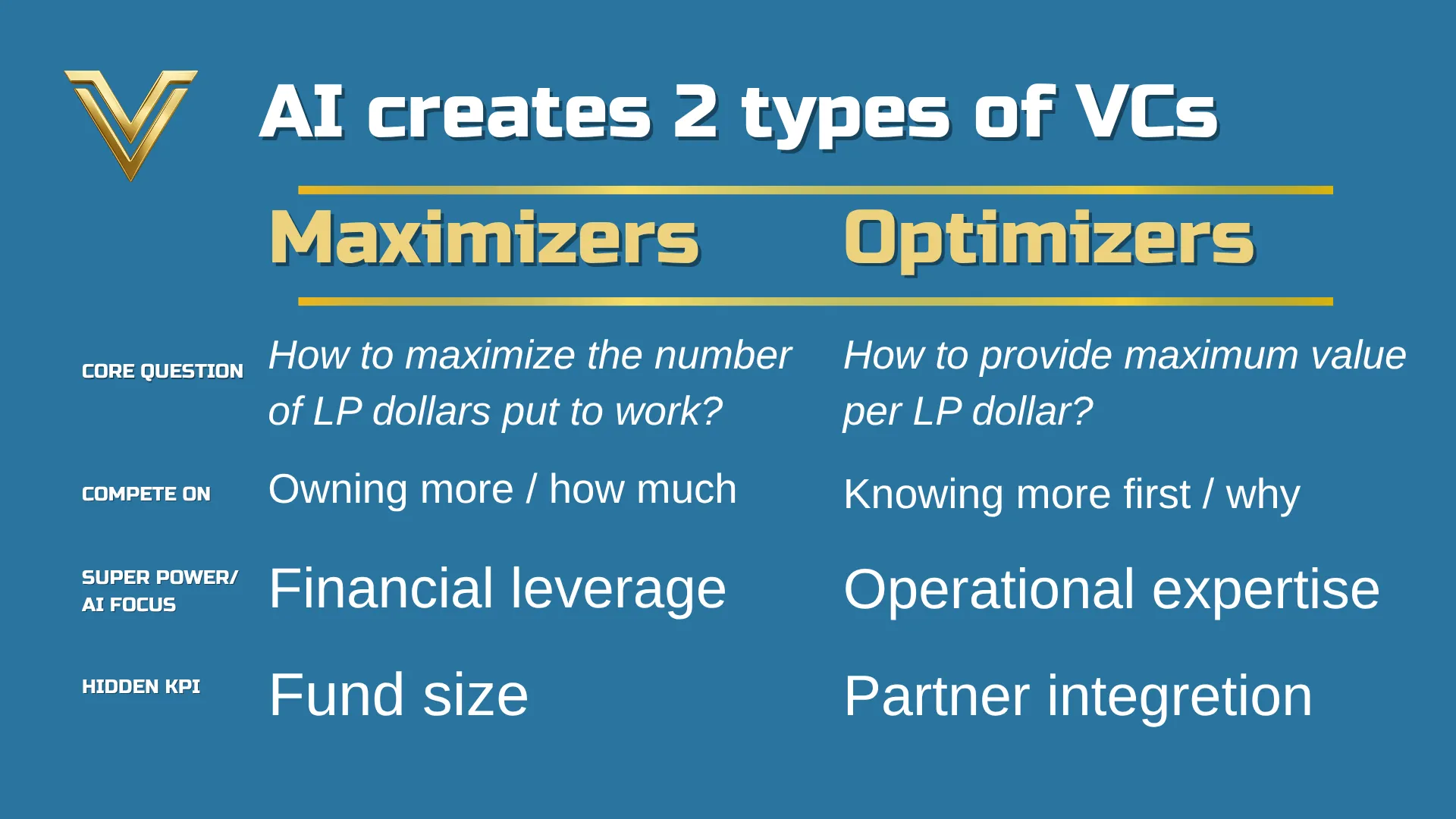

In February ("AI Creates 2 LP/GP Models") I shared that AI was not creating "legacy vs. emerging" VC. It was creating something more structural: maximization vs. optimization — two different answers to two different questions.

How many dollars do you need to be powerful? vs.

How powerful can your dollar be, in the right process?

Here's a brief recap of the positions:

One quarter later, the data has stopped being a forecast. The split is now visible in the print, not just the posture.

For team Maximizer, the Q1 venture headline looks healthy: U.S. quarterly deal value of $267.2B and exit value of $347.3B, both records (PitchBook-NVCA, Apr 2026).

However, strip the five largest deals and that figure collapses by 73%.

Strip the top five exits and exit value collapses 87%.

Four companies — OpenAI, Anthropic, xAI, and Waymo — absorbed roughly two-thirds of global venture dollars. On the LP side, 73% of capital raised in Q1 went to only five firms (per SaaStr / KPMG Venture Pulse, Apr 2026).

Underneath the headline, the market the Optimizers of venture were built for, firms like Valor, is the healthiest it has been in a decade.

Trailing-twelve-month SaaS M&A reached 2,723 transactions — the most active period Software Equity Group has ever recorded.

Median EV/TTM revenue in private SaaS M&A printed at 6.3x, SEG's second-highest reading on record.

55% of Q1 SaaS M&A landed in vertical software, and top-quartile AI-native vertical assets cleared 9–18x ARR (SEG, Apr 2026; Houlihan Lokey, AI in Vertical Software, Q1 2026).

The Maximizer thesis | The Optimizer thesis |

|---|---|

73% of Q1 LP capital went to just 5 firms¹ | 2,723 SaaS M&A deals TTM — the most active period SEG has ever tracked² |

~2/3 of global VC dollars flowed into 4 megadeals: OpenAI, Anthropic, xAI, Waymo¹ | 6.3x median EV/TTM revenue in private SaaS M&A — SEG's 2nd-highest reading on record² |

$267B U.S. quarterly deal value — collapses 73% if you strip the top 5 deals¹ | 55% of Q1 SaaS M&A landed in vertical software, up from 49% YoY² |

3.6x median public SaaS EV/TTM revenue — a decade-plus low; SEG SaaS Index down ~25% in Q1² | 9–18x ARR clearing for AI-native vertical assets; top platforms 16–18x²,³ |

$347B exit value — collapses 87% ex-top-5¹ | 13.6% all-time-high median EBITDA margin in public SaaS — the model works; only the risk premium is being repriced² |

5 firms = the entire fundraising story for thoughtful LPs⁴ | 60% of Q1 SaaS M&A involved PE/VC-backed buyers — the bid is structural, not episodic² |

Sources: ¹PitchBook-NVCA Venture Monitor, Q1 2026. ²Software Equity Group, 1Q26 SaaS M&A and Public Market Report, Apr 2026. ³Houlihan Lokey, AI in Vertical Software — Market Update Q1 2026; SaaS Capital, "Four Early 2026 SaaS Trends," Apr 2026. ⁴SaaStr / KPMG Venture Pulse synthesis, Apr 2026.

The left column is concentration. The right column is craft.

Both can be true, but the VCs lined up on either side of this split answer different questions for LPs. Three things got clearer in Q1 and this can help sophisticated investors making their allocation choices in the year or two ahead:

Liquidity is being earned in vertical M&A, not in the IPO window. Sub-billion SaaS IPOs remain effectively closed. M&A is doing the work, and the cohort clearing at premium is exactly the cohort an Optimizer firm builds toward on purpose: vertical, AI-augmented, workflow-embedded, with strategics already paying for embeddedness.

The South is now pricing into the exit math. In the South, average check sizes up 45%+ since 2018 — fewer deals, bigger checks, higher operating bar. North Carolina closed >$2B in 2025; Atlanta closed $4.3B across 380+ deals. The operating discipline that has been a Southern feature for a decade is what acquirers are now underwriting at 9–18x.

Optimizer compounds; Maximizer accumulates. When LP capital concentrates into five firms and four assets, fee income concentrates with it — and so does correlation. The Maximizer LP outcome rides on a small number of names that may (or may not) be a bubble.

Where Valor stands

Valor is firmly in camp Optimizer, and Q1 made that structural rather than stylistic. Our harvest-stage portfolio is sitting on the side of the multiple distribution we see the market paying up for. We have our work cut out for us making sure the right strategics know about the stars in Valor's growing portfolio, and if you have a referral for us, always appreciate the support.

— Lisa